When opening or maintaining U.S. bank accounts, whether checking, savings, investment, or business banking, you almost always need a stable, verifiable U.S. address. For many people, especially digital nomads, remote workers, and international residents, a U.S. home address is the most reliable option to satisfy banking and regulatory requirements.

This guide explains:

- What banks require for address verification

- When a home address works

- What address types won’t work

- How to set up an address that passes compliance

What banks mean by a 'home address'

In simple terms, a home address is your permanent residential address. It is the place where you live, receive mail, and legally reside. For U.S. banking purposes, it shows a fixed point of contact that banks can use for communications and compliance checks.

Banks rely on your home address for:

- Identity verification (part of Know Your Customer or KYC rules)

- Regulatory compliance, including anti-money-laundering (AML) safeguards

- Sending statements, notices, and secure documents

- Contacting you if there are issues with your account

Without a valid home address on file, a bank may flag, suspend, or even freeze your account.

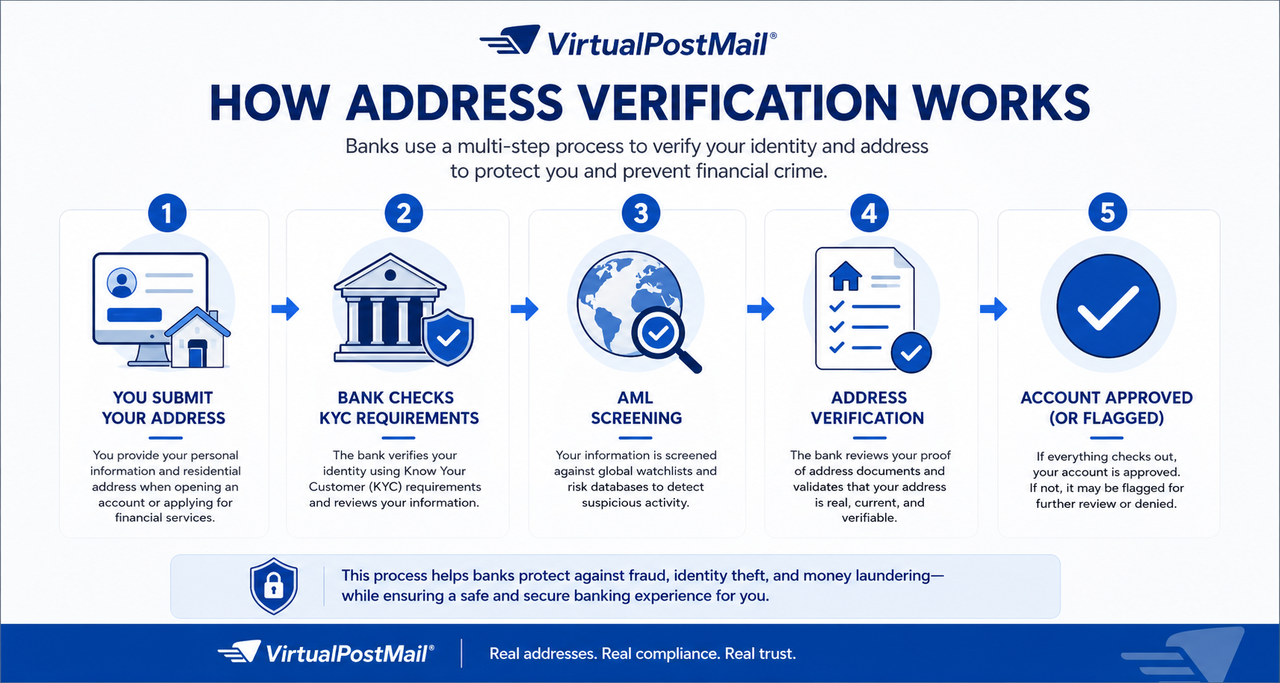

Know Your Customer (KYC) laws and why they matter

Know Your Customer (KYC) laws are a set of regulations that require banks to verify the identity of their customers before providing services or opening an account. These laws are part of a broader effort to combat illegal activities, such as money laundering, fraud, terrorist financing, and other financial crimes. KYC regulations help ensure that financial institutions know exactly who their customers are, reducing the risk of criminal activities.

KYC compliance typically involves collecting and verifying key personal information, including:

- Full name

- Date of birth

- Physical address

- Social security number

- Government-issued ID (i.e., driver’s license, passport)

- Proof of address (usually in the form of a lease agreement)

How do Anti-Money Laundering (AML) laws tie into banking?

Anti-Money Laundering (AML) laws play an important role in safeguarding your banking and financial accounts. While KYC procedures focus on verifying your identity, AML regulations go beyond that by actively monitoring financial transactions to detect and prevent suspicious activities, such as money laundering, terrorist financing, or tax evasion.

KYC is the first line of defense in the AML process. By confirming your identity and assessing your risk, banks can spot potential red flags early on. After your identity is verified, AML measures like transaction monitoring and suspicious activity reporting (SAR), continue to protect your accounts, ensuring they aren’t being used for illegal activities.

Having a stable U.S. address helps you stay compliant with these regulations, keeping your financial accounts secure as you travel. A home address, in particular, reassures financial institutions that you’re a legitimate customer, making it easier to navigate both KYC and AML requirements while abroad.

When a home address can be used for banking

A home address generally works for:

- Opening personal or business bank accounts

- Address verification for credit and identity checks

- Receiving mailed banking notices and documents

Using your home address does not change your legal liability or corporate structure, it’s a record-keeping requirement. In most U.S. states, sensitive information like this remains private in bank records and is not public.

What counts as valid proof of your home address

To verify a home address with a bank, you often need documents that show your name and address clearly. Common examples include:

- Utility bills (electricity, water, internet)

- Mortgage statements or lease agreements

- Bank or credit card statements

- Driver’s license, state ID, or government mail

These documents give the bank tangible evidence that the address you provided is real, stable, and tied to you.

Finding the right residential address for banking and verification

Not every address will qualify as your official “home address” for banking purposes. To satisfy traditional banking and regulatory standards (keep in mind that online banks and fintechs may differ), your home address needs to meet the following conditions:

- It’s a reliable, long-term residence. Your home address should be linked to a tangible place in which you have a permanent right to reside, such as a primary home, apartment, or other residential property (i.e. a brick-and-mortar location).

- It’s used for tax and legal purposes. To be considered a home address, it should be used for registration purposes, like tax filings and/or your driver’s license.

- It’s not a virtual address, PO box, or mailbox service. Banks typically won’t accept virtual offices, coworking spaces, PO boxes, or commercial mailbox services as valid home addresses.

Understanding these requirements is the first step to meeting banking regulations, but it's also important to know how address verification ties into broader consumer protections.

| PO Box | |||

| Virtual Mailbox | |||

| Friend or Relative’s Address | |||

| Co-working/Virtual Office | |||

| Residential Address Solution |

The advantages of using a home address for banking

Home addresses offer easier verification and fewer regulatory hurdles, making them a more ideal option for maintaining and opening your U.S. financial accounts.

Let’s take a closer look at why a home address is essential for keeping your financial accounts in good standing.

Home addresses are easier for new account verification

You’re probably wondering why home addresses are preferred for financial accounts. For starters, they require less documentation. Business addresses are considerably more likely to trigger additional verification requirements due to KYC and AML laws. They tend to fall under a high level of scrutiny, and since a business address can come in many different forms, banks must vet the address thoroughly to make sure they aren't linked to virtual offices, coworking spaces, or PO boxes.

Home addresses are seen as more straightforward, and therefore it is considerably easier for them to pass the verification stage.

Home addresses can be used when you’re traveling

As a digital nomad, maintaining a valid home address for personal accounts can be challenging.

However, even if you’re temporarily residing away from your home address (i.e. you are working, traveling, or studying abroad), you can still use it for banking, as long as it’s your legal permanent address. Banks recognize that people often move around, so using a stable home address provides a consistent point of contact, regardless of your location.

Additionally, using a stable home address can help you avoid potential red flags during the verification process that could arise if you frequently change addresses or use temporary locations (i.e. a friend or family member’s address).

Why other types of addresses fall short for banking

While it might be tempting to use a virtual mailbox, virtual office, coworking space, or PO box for convenience, these options are often flagged as unacceptable for financial verification purposes. Why? Because they lack the stability and authenticity that banks require to comply with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations.

Virtual mailboxes weren’t made for banking

Virtual mailboxes are particularly problematic because they’re classified as Commercial Mail Receiving Agencies (CMRAs) in the USPS system. This designation alerts banks that the address is tied to a third-party mail service rather than a legitimate, fixed business location. Since CMRAs are designed to receive and forward mail rather than serve as an actual operating address, banks typically reject these addresses outright, viewing them as unreliable and non-compliant for financial verification.

This type of rejection isn’t just limited to traditional banks; many online banks and fintechs, while sometimes more lenient, still need to follow basic compliance standards. Using a virtual mailbox can quickly complicate the application process, trigger additional scrutiny, or even result in account closure if discovered after the fact.

Virtual offices, coworking spaces, and PO boxes aren’t much better

A virtual office or coworking space might seem like a viable option since these are typically physical addresses. However, banks see these setups as temporary or non-permanent, which raises concerns about the legitimacy and stability of your business.

PO boxes are almost universally rejected by banks as they provide no way to verify your business’s physical presence. Banks view PO boxes as impermanent and untraceable, making them unsuitable for compliance and verification purposes. Even if you use a private mailbox service that offers a street address format (e.g., “Suite #123” instead of “PO Box 123”), these addresses are still treated as CMRAs and are likely to be declined.

If your address is flagged in the system, the bank may ask for additional proof, such as a signed lease agreement, utility bill, or even business registration documents to verify that you have an active, exclusive presence there. But in many cases, this won’t be enough, and your application will be denied.

You may have to provide additional proof of address

Many banks will want to see something more concrete than just your business address. This is the biggest reason why the types of addresses mentioned above (i.e. a virtual mailbox, coworking address, or PO box) are typically rejected.

The most commonly accepted proof of address documents include:

- Lease agreement: A signed lease agreement under the business’s name is one of the strongest forms of proof. It demonstrates that your business has a long-term, verifiable presence at that location.

- Utility bill: A utility bill (i.e., water, electricity, or internet) linked to the address can also validate your physical presence.

Without these additional documents, there’s a good chance that the bank may request further verification or even reject your application altogether. This is particularly common if your address raises red flags during the initial review.

A home address makes it easier to provide proof of address when required, often through utility bills or other official documents sent to that location.

What to do if you don’t have a U.S. home address

If you don’t have a U.S. residence, you generally have two options:

- Use a compliant address: In some situations, a leased commercial or residential address in the U.S. that you can verify with utility bills or lease agreements may work.

- Ask the bank directly: Some banks or fintechs may accept alternate forms of verification or foreign addresses depending on their policies.

Choose a stable address for your banking needs

To steer clear of complications while managing your U.S. accounts, selecting a home address is your best bet. With VPM’s TruResidence service, you can secure a prestigious home address for all your personal banking needs, along with seamless mail management, no matter where you are in the world. Sign up today to stay connected and compliant, ensuring your banking remains hassle-free as you travel.